Why A Flattening Yield Curve Is Worth Noting

Several people have asked us why there is currently so little difference between our current 24 Month Certificate rate (3.00%) and our 36 Month rate (3.20%), our 48 Month (3.30%) and our 60 Month (3.40%) rate. The short answer is that following the Federal Reserve’s interest rate hike in June, we surveyed major banks to find out what they were offering and modeled our new rates on theirs, albeit at more attractive rates. Our objective is always to offer rates that are higher than those offered by major or local banks.

But you may be asking “Is there anything I should ‘read’ into this set of rates?” The answer to that is a big, fat “Maybe!” For 18 months or so, the difference between long term rates and short term rates has been narrowing. This is referred to in the industry as a flattening of the yield curve.

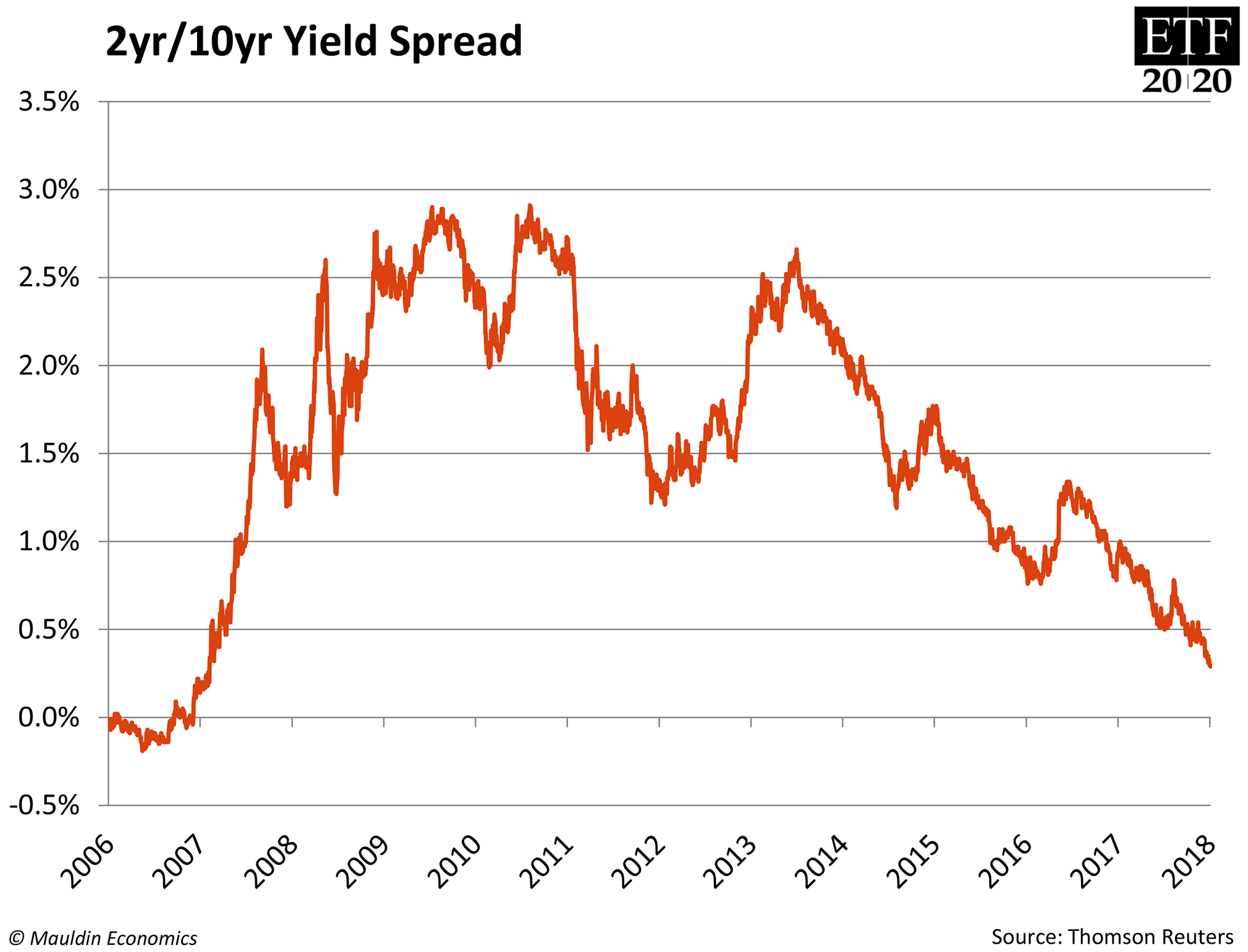

One of the most common figures that bankers watch is the difference between the yield on 10 year Treasuries and 2 year Treasuries. At the end of 2016, that difference was 123 basis points (bps) or 1.23%. At the end of 2017, the difference had shrunk to 59 bps or 0.59%. At the end of April it was 46 bps and at the end of last month it was only 30 bps.

At various points in the past, the difference has actually gone negative or the yield curve has “inverted”, i.e. the rate on the 2 year Treasury was actually higher than the rate on the 10 year Treasury. Why is that important? Because virtually all of the recessions of the last 50 – 75 years have been preceded by a flattening or inverted yield curve 6 – 12 months earlier.

Does this mean we’re going to have a recession soon? Not necessarily. There are a lot of good reasons to argue that this time, it will be different. However, we are about to break the record for the longest bull run in American history – more than 10 years and to say that we’re “overdo” for a recession would not be a stretch.

We’ll continue to keep an eye on this important metric and try to keep you informed of the progress. In the meantime, savvy investors may want to survey their holdings and consider taking some profits an holdings that have performed very well for you. My good friend Jim Cramer says that no one ever cries while taking their profits to the bank!